Having a Roth IRA account in place for retirement is a responsible plan for the future. After all, you wouldn’t want to worry about your financial security when you’ve finally reached an age to enjoy the fruits of your labor.

If you’re contributing to this type of retirement account, you might be wondering what Roth IRA withdrawal rules are in place. Luckily, tax experts are available to help answer any questions along the way, especially with a topic so complex.

You’re always eligible for tax- and penalty-free withdrawals on contributions, but you must meet certain Roth IRA rules for withdrawal to withdraw earnings. There are rules for withdrawal both at the time of retirement and sooner if you were to need extra money immediately. Use this guide to learn more about the withdrawal rules for Roth IRAs.

Some key takeaways for a Roth IRA withdrawal include:

- Roth IRA distributions on contributions can be taken at any time, both tax- and penalty-free.

- Roth IRA distributions on earnings can be taken both tax- and penalty-free when:

- You’ve reached the age of 59.5, and

- Your Roth IRA account has been open for five years

- The taxes and penalties might be avoided during certain situations, including purchasing your first home, birth or adoption, or covering college education expenses.

Keep reading to learn more about the Roth IRA retirement account, including detailed information on withdrawals and certain limits on contributions.

Are you allowed to withdraw Roth IRA contributions?

It’s important to make this distinction when talking about rules for withdrawing from a Roth IRA: You can withdraw contributions that have been made to your Roth IRA at any time, both tax- and penalty-free. However, depending on when you withdraw your Roth IRA earnings, you might have to pay taxes and penalties.

If you’re withdrawing Roth IRA earnings, to avoid triggering a 10% early withdrawal penalty, you must be at least 59 ½ years old, and your account must be open for a minimum of five years. Once you’ve reached this point, you can make tax- and penalty-free withdrawals on your Roth IRA earnings.

Roth IRA Contributions and Earnings

It’s important to make this distinction when talking about Roth IRA withdrawal rules: You can withdraw contributions that have been made to your Roth IRA at any time, both tax- and penalty-free. However, depending on when you withdraw your Roth IRA earnings, you might have to pay taxes and penalties.

What are qualified vs. nonqualified distributions?

Qualified and nonqualified distributions determine whether there are taxes and penalties when you withdraw earnings from your Roth IRA. For qualified Roth IRA distributions, you must be at least 59 ½ years old, and your Roth IRA must be at least 5 years old.

If you decide to make a withdrawal on Roth IRA earnings before your account has been open for five years, you may have to pay income taxes and a 10% penalty.

Keep in mind that certain circumstances can protect you from Roth IRA penalties and taxes. For example, you can withdraw up to $10,000 if you’re purchasing your first home.

What are the Roth IRA withdrawal rules?

Before withdrawing from a Roth account, it’s necessary to understand the rules and limitations associated with distributions. Contributions to a Roth IRA are not tax-deductible, though earnings can grow tax-free. Qualified distributions are both tax and penalty-free, while non-qualified distributions will incur penalties depending on different factors.

Keep the following Roth IRA withdrawal rules in mind to avoid a 10% early withdrawal penalty:

- Withdrawals must be taken after you’ve turned 59.5 years old.

- Withdrawals must be taken after your five-year waiting period.

There are certain exceptions to the early withdrawal penalty — these include distributions to fund certain expenses, like:

- Purchasing your first home

- Birth

- Adoption

- College tuition

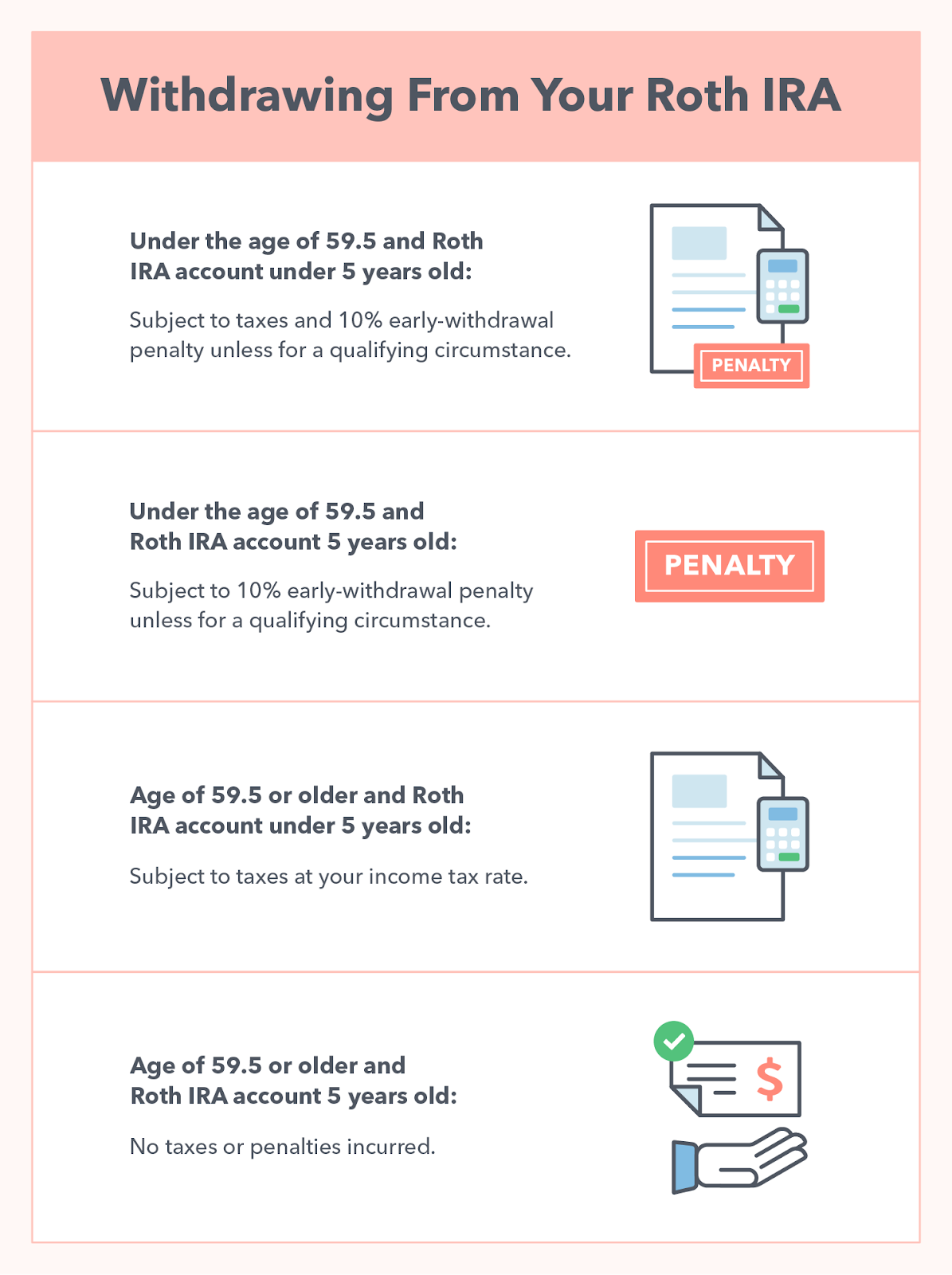

Roth IRA withdrawal rules for those under the age of 59.5

If you’re under the age of 59.5, you might need to pay taxes and penalties on your earnings that you’d like to withdraw from your Roth account. Remember that you can withdraw your contributions at any time without taxes or penalty; these only apply to the earnings on your account.

- If you’ve had your Roth IRA for less than five years: You will be subject to both your standard income tax rate and a 10% penalty on your earnings distribution. You might be able to steer clear of the 10% penalty if you use the funds for one of the following situations:

- Permanent disability

- First home purchase

- Qualified education expenses

- The birth or adoption of a child

- Substantially equal periodic payments

- Unreimbursed medical expenses or health insurance if you lose your job

- If you’ve had your Roth IRA for more than five years: You won’t be subject to taxes, but you will incur a 10% early-withdrawal penalty. You might be able to avoid the 10% penalty if you meet one of the following circumstances:

- Permanent disability

- First home purchase

- Qualified education expenses

- The birth or adoption of a child

- Substantially equal periodic payments

- Unreimbursed medical expenses or health insurance if you lose your job

Roth IRA withdrawal rules for those over the age of 59.5

If you’ve reached the age of 59.5, you’ve met half of the requirements to withdraw your Roth IRA earnings both tax- and penalty-free. The second half of the requirement is the Roth IRA Five-Year Rule.

- If you’ve had your Roth IRA for less than five years: Your earnings will be subject to taxes at your normal tax rate, but you won’t be subject to the 10% penalty.

- If you’ve had your Roth IRA for more than five years: You can withdraw your Roth IRA earnings with no taxes and no penalties.

Based on the above scenarios, the best time to withdraw from your Roth IRA account is when you’ve had your account for five years or more and have reached the age of 59.5. This will help you make the most of your contributions and earnings.

The distributions that you take once you’ve reached both milestones (or a qualifying event) are known as qualified distributions. Otherwise, the distributions are considered non-qualifying distributions.

Exceptions to the Roth IRA withdrawal rules

While there are several rules for Roth IRA withdrawals, there are also exceptions. Under certain circumstances, you may be able to make tax- and penalty-free withdrawals.

If you’re purchasing your first home with earnings from your Roth IRA, you can withdraw up to $10,000 from your Roth IRA without facing penalties. Keep in mind that this penalty-free withdrawal only applies when you’re buying your first home.

You can also use Roth IRA earnings to pay for expenses related to higher education, including college tuition and other fees. As long as you’re covering qualified education expenses, you don’t have to worry about an additional 10% penalty but typically early withdrawals of earnings are subject to income taxes.

Roth IRA five-year rule

With a Roth IRA account, there are two requirements that must be met if you wish to withdraw your earnings without owing any taxes and penalties: You must be 59.5 years of age or older, and you must satisfy the five-year rule.

So, what exactly is the five-year rule? This rule states that there must be five years between the time you make your first contribution and the time that you withdraw your earnings. This rule applies regardless of age, even if you were to hit the age of 59.5 in the meantime.

If you choose to withdraw your Roth IRA earnings before you’ve satisfied this five-year rule, expect to pay taxes on the withdrawal as well as a 10% Roth IRA early-withdrawal penalty.

Roth IRA contribution limits

The annual amount that you’re allowed to contribute to your Roth IRA is limited by the income that you earn. The annual Roth IRA contribution limit is $6,500 for 2023; this changes to $7,500 if you’re 50 or older. For 2024, the Roth IRA contribution limit is $7,000 (or $8,000 if you are 50 or older). In other words, your contributions to your Roth IRA account can’t exceed this limit.

Roth IRA income limits

Similarly to the contribution limits, certain limits on income exist with regard to a Roth IRA account.

- If you’re a single filer or head of household: Your Modified Adjusted Gross Income (MAGI) must be less than $153,000 in 2023 ($161,000 in 2024).

- If you’re a joint filer: Your MAGI must be less than $228,000 in 2023 ($230,000 in 2024).

So, what do these numbers mean? If your income exceeds the upper limit, you can’t contribute to a Roth IRA account. As the amount of money you make increases, your maximum contribution amount decreases.

Below is additional information on how the limits for 2023 and 2024 are calculated:

- Single or head of household filing status:

- 2023 MAGI: less than $138,000

- Maximum annual contribution: $6,500 (or $7,500 if age 50 or older)

- 2024 MAGI: less than $146,000

- Maximum annual contribution: $7,000 (or $8,000 if age 50 or older)

- 2023 MAGI: $138,000 to $152,999

- Maximum annual contribution: Reduced

- 2024 MAGI: $146,000 to $160,999

- Maximum annual contribution: Reduced

- 2023 MAGI: $153,000 or more

- No contribution allowed

- 2024 MAGI: $161,000 or more

- No contribution allowed

- 2023 MAGI: less than $138,000

- Married filing jointly or qualifying widower filing status:

- 2023 MAGI: less than $218,000

- Maximum annual contribution $6,500 ($7,500 if age 50 or older)

- 2024 MAGI: less than $230,000

- Maximum annual contribution $7,000 ($8,000 if age 50 or older)

- 2023 MAGI: $218,000 to $227,999

- Maximum annual contribution: Reduced

- 2024 MAGI: $230,000 to $239,999

- Maximum annual contribution: Reduced

- 2023 MAGI: $228,000 or more

- No contribution allowed

- 2024 MAGI: $240,000 or more

- No contribution allowed

- 2023 MAGI: less than $218,000

As you can see, Roth IRA accounts typically favor those in a lower income bracket, as they can contribute the most. As you climb the income bracket level, the amount that you can contribute evens out to zero.

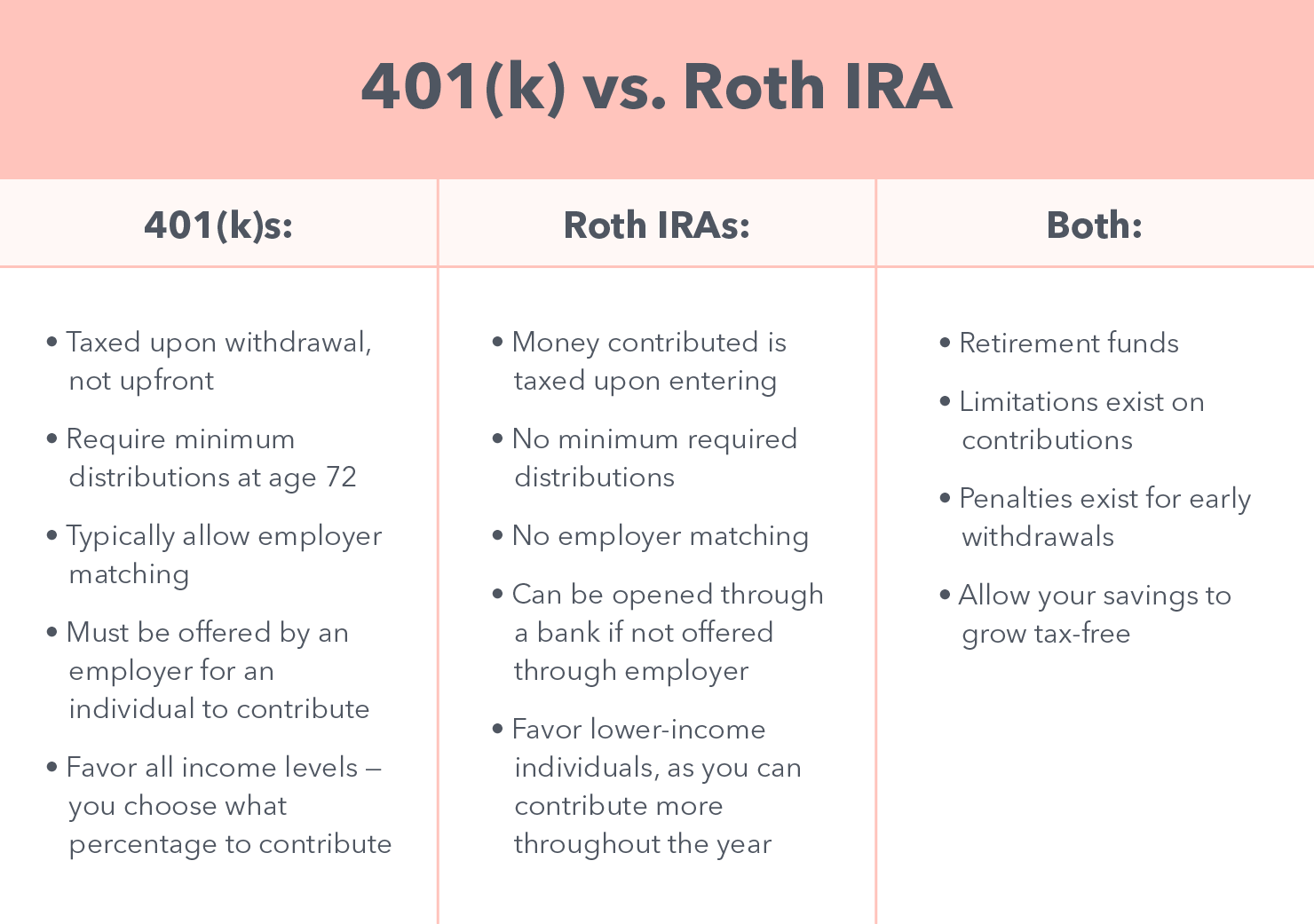

401(k) vs. Roth IRA

When discussing retirement plans, you might hear about both Roth IRAs and traditional 401(k)s. While these are both great options to help you save for retirement, there are plenty of differences between these two plans that make them unique.

A traditional 401(k) plan is tax-deferred, meaning that the money that is contributed is not taxed upon entering but is taxed when distributed. In addition:

- Employers can offer to match a percentage of your contribution and add it to your 401(k) account.

- 401(k)s require minimum distributions starting at age 72.

- Employers must offer the 401(k) program in order for an individual to contribute.

Roth IRA plans are a little different, specifically in the way that taxes work. Roth IRA contributions are taxed as they enter the plan, making them untaxed as they are withdrawn. In addition:

- Roth IRAs can be opened even if an employer does not offer them.

- There are no required minimum distributions to a Roth IRA.

- Roth IRAs favor those making a lower income, as they can contribute more per year.

Although there are several differences, there are a few ways they are the same. For starters, limitations exist on contributions, though the limit for 401(k) is much higher. In addition, both plans impose a penalty for a nonqualified early withdrawal.

Pros and cons of taking a Roth IRA withdrawal

While it might be tempting to take a Roth IRA withdrawal, ideally, you should wait to withdraw until retirement. At this point, you’ve likely satisfied both the five-year rule and the minimum age of 59.5. After all, the longer you wait, the more you can maximize your overall contributions and earnings. This provides you with more money for the future without paying any potential penalties.

It’s important to note before you withdraw from a Roth IRA that money can’t be repaid to the account. Once it’s gone, that money and any earnings that would have come with it are also gone.

If there’s a situation where you need to withdraw from your Roth IRA, it’s best to consider the pros and cons first. By withdrawing your Roth IRA, you can avoid paying interest on a loan. This saves you money in the long run.

In addition, you can always take out your contributions both tax and penalty-free and, in some cases, withdraw your earnings penalty-free as well. This may provide you with immediate cash relief when you need it the most.

Before withdrawing, however, it’s important to know there are a few drawbacks as well. First, the money can’t be repaid to the account, meaning that you’re missing out on future tax-free growth. In addition, if you were to withdraw your earnings, you’ll incur taxes and penalties if you haven’t had the account for five years and you’re under 59.5 years old.

Lastly, and maybe most importantly, any money you withdraw now won’t be available to you later in life when you retire. This might make this situation financially difficult for you.

Do I have to report my Roth IRA withdrawal on my tax return?

Roth IRA contributions are made with after-tax dollars, and those contributions aren’t tax-deductible. Qualified distributions also aren’t considered taxable income. So you won’t report Roth IRA contributions or qualified distributions on your tax return. However, if you receive a non-qualified distribution from your Roth IRA you will have to report that distribution to the IRS. This is one of the reasons Roth IRAs are such a popular retirement option.

The short answer is that you don’t have to report contributions on your tax return.

Alleviate stress with tax help

Understanding Roth IRA withdrawal rules doesn’t have to be a difficult process. Meet with a TurboTax Full Service expert who can prepare, sign, and file your taxes. That way, you can be 100% confident your taxes are done right.

No matter what moves you made last year, TurboTax will make them count on your taxes. Whether you want to do your taxes yourself or have a TurboTax expert file for you, we’ll make sure you get every dollar you deserve and your biggest possible refund – guaranteed.