Untangling tax laws can feel like navigating a maze, especially when you’re trying to decipher what feels like an entirely new language. When filling out your tax form, one term that used to play a major role in individual tax returns was “personal exemption.”

This exemption allowed individuals to deduct a specific amount from their total income when figuring their taxable income while completing their tax forms. It played a vital role in shaping tax liabilities and influencing financial strategies.

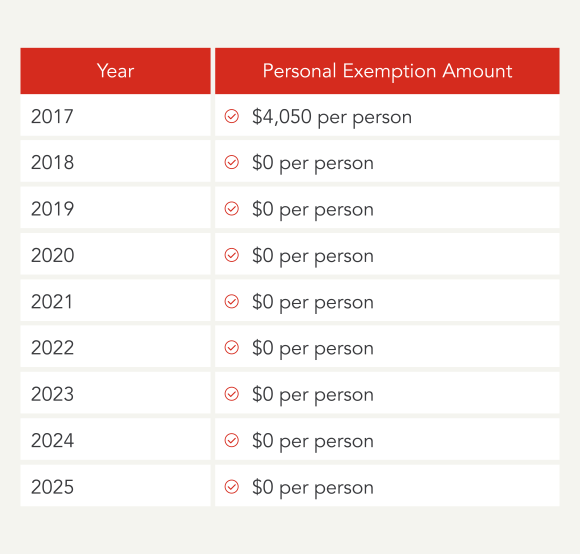

However, tax law changes have been quite significant and the Tax Cuts and Jobs Acts in 2017 eliminated this exemption. Now, that might change in 2025, but for tax year 2023, there are no personal exemptions.

This major shift has likely changed how you approach your taxes. To help you get a better understanding of their impact, let’s take a look at the historical role of personal exemptions and what their absence means for current tax planning.

What is a personal exemption?

A personal exemption was a fixed deduction that was subtracted from your total income. You and each member of your family were entitled to one personal exemption. These personal exemptions would reduce your total taxable income.

The personal exemption helped reduce the burden of financially supporting yourself and dependents by reducing taxable income. However, there were a few exceptions. For example, if you could be claimed as a dependent, you couldn’t claim the personal exemption.

Even if you qualified for a personal exemption, it didn’t mean you were able to claim the full amount. Based on your adjusted gross income (AGI), you would begin to phase out at a certain threshold.

In the 2017 tax year, if a single filer’s AGI was above $261,500, the personal exemption was reduced. It would phase out completely for an AGI above $384,000.

Significant changes occurred with the implementation of the Tax Cuts and Jobs Act, signed into law in 2017. As a result, individuals could no longer claim a specific dollar amount as a personal exemption for:

- Themselves

- Their spouses

- Their dependents

What is the personal exemption for 2024?

In 2024, the personal exemption continues to stand at $0. This is due to the provision enacted in 2017 through the Tax Cuts and Jobs Act.

The personal exemption isn’t applicable for tax returns beginning after December 31, 2017, and before January 1, 2026.

How did the Tax Cuts & Jobs Act affect personal exemptions?

The Tax Cuts and Jobs Act was signed in 2017 and went into effect in 2018 (for the tax year of 2017.) Some of the provisions included in the bill will revert back after 2025 unless extended. Key changes include new tax rates, increased standard deductions, and updates to various deductions such as:

- State and local taxes

- Mortgage interest

- Charitable contributions

The child tax credit was expanded, and the “kiddie tax” has new criteria. Notable changes also affect:

- Alimony

- Alternative Minimum Tax (AMT)

- Obamacare mandate penalties

- Treatment of 529 Plan funds

Understanding these changes is crucial for navigating the evolving tax landscape.

Among the other tax law changes, the Tax Cuts and Jobs Act eliminated personal exemptions starting after December 31, 2017, until January 1, 2026. Prior to the Act, taxpayers could deduct a personal exemption for:

- Themselves

- Their spouse

- Each dependent from their adjusted gross income

How have personal exemptions worked in the past?

In the past, personal exemptions were applied to each individual and the dependents that each individual could claim on their tax return.

Typically, each individual was entitled to one personal exemption for themselves. This only applied if they could not be claimed as a dependent on another taxpayer’s return. For the tax year of 2017, the personal exemption stood at $4,050 per person.

A dependent is a qualifying child or relative. See the past guidelines listed below.

Qualifying children under the old personal exemption rules

For a qualifying child:

- The eligible child would have needed to fall under one of these categories: your son, daughter, stepchild, foster child, brother, sister, half-sibling, step-sibling, or a descendent of any of them.

A child that was legally adopted would’ve also qualified.

- Specific age criteria should’ve applied: the child is either under 19 years old at the end of the year and younger than you or a full-time student under 24 years old at the end of the year and younger than you.

A child that was permanently and totally disabled would’ve qualified regardless of age.

- The child must have resided with you for more than half of the year. Exceptions existed for temporary absences due to illness or travel, newborns or deceased children during the year, kidnapped children, and those of divorced or separated parents.

- The child cannot have provided more than half of their own support for the year, including basic needs such as room and board.

- The child cannot have filed a joint tax return with any other person for the year.

Claiming a child under the old personal exemption rules

In cases where two taxpayers both believed a child qualified under the preceding criteria, special tie-breaker rules would’ve apply:

- If only one taxpayer was the child’s parent, they’re treated as the qualifying child of that parent.

- If both parents claimed the child but filed separately, the IRS considers which parent lived with the child the longest during the tax year.

- If the time was equal, the child would’ve been treated as the qualifying child of the parent with the higher adjusted gross Income (AGI).

- If no parent was claiming the child, they’re treated as the qualifying child of the taxpayer with the highest AGI.

- If no parent claimed the child, and they were eligible to do so, the child would’ve been treated as the qualifying child of the taxpayer with the highest AGI, provided it surpasses that of any eligible parents.

If all else failed, the taxpayers could have reached an agreement between themselves regarding who may claim the child.

Qualifying relative under the old personal exemption rules

This is also known as the “not qualifying child test.” The following criteria must’ve applied:

- A child cannot have been your qualifying relative if they already qualified as the qualifying child of another taxpayer.

- Your relative must have fulfilled one of two conditions: either resided with you throughout the entire year as a household member or have a specified relationship with you. While immediate family members naturally meet this requirement, it also encompasses half-siblings, step-siblings, and in-laws.

- The relative’s gross income for the year must not have exceeded the income threshold of the tax year.

- You must have contributed more than half of your relative’s total support during the year to meet this criterion.

In order to officially claim a dependent as a personal exemption on your tax return, you must have provided:

- Their name

- Social Security number

- Relationship to you

If you’re using tax preparation software or a tax professional, you likely had to provide the birth dates of your dependents.

In addition, personal exemptions could have also applied to married couples. For a married couple who filed a joint income tax return, an exemption could have been claimed for the spouse.

If you were married and filing a separate tax return, the exemption could have be claimed for the spouse under the conditions that the spouse:

- Had no gross income

- Wasn’t filing a tax return

- Couldn’t have been claimed as a dependent by someone else

What is the difference between an exemption vs. deduction?

Although both exemptions and deductions reduce your total taxable income, they differ from one another in significant ways.

The number of exemptions you could have qualified for depended on your filing status and the number of dependents you had. On the other hand, now you either claim a standard deduction or an itemized deduction. deductions are tied to your expenses. When you claim a standard deduction it is arguably easier because you don’t have to keep track of expenses and you take standard deduction for your filing status. The 2023 standard deduction is $13,850 for single taxpayers ($20,800 if you are filing head of household or $27,700 for those married filing jointly). Some common examples of deductions for those itemizing deductions include student loan interest deduction if you’re repaying student loans, contributions to qualified charitable organizations, or interest paid on your home mortgage.

The standard deduction for single filers was $6,350 in the tax year 2017 when personal exemptions were still allowed.

How can you lower your tax bill?

When it comes to taxes, there are plenty of nuances that make it difficult to navigate tax laws. Although you can’t use a personal exemption now, there are still other ways to save on your taxes and increase your tax refund.

Here are a few tips to ensure maximum savings come tax time:

Understand deductions

Effectively utilizing deductions is crucial to minimizing your tax bill. Identify any eligible expenses, maintain accurate records, and choose between itemized and standard deductions based on maximum benefit. Strategically time deductible expenses and leverage tax-advantaged accounts to reduce taxable income.

There are a number of itemized deductions to consider looking into, such as:

- Medical and dental expenses

- Combined total of state and local income taxes

- Mortgage interest

- Charitable contributions

- Casualty losses during a nationally declared disaster

Contribute to retirement

You can lower your tax bill by reducing your taxable income. One strategic move is reaching the maximum contribution amount for pre-tax plans like a 401(k) or IRA.

You may want to consider converting your traditional IRA to a Roth IRA. Unlike a traditional IRA, converted amounts from a Roth IRA typically don’t incur federal income taxes on qualified distributions, provided that:

- A minimum of five years has passed since your initial Roth IRA contribution or conversion.

- You are 59½ or older.

Explore different investment strategies

You might want to look into putting some of your income toward investments. With a buy-and-hold strategy, you can enjoy deferred capital gains.

Note that if your modified adjusted gross income reaches $200,000 or more ($250,000 or more if married filing jointly), you are liable for a 3.8% Net Investment Income Tax (NIIT). Depending on which is lower, this will apply to either:

- Your net investment income

- The amount of your modified adjusted gross income (MAGI) that surpasses the $200,000 threshold for single or head of household ($250,000 for married filing jointly)

Note that specific exclusions apply, so you’ll want to consult your tax advisor.

Embrace clean energy

Enacted in 2022, The Inflation Reduction Act allocated billions for clean energy tax credits and other efforts to address climate change. As an individual, something to note is the potential for substantial tax credits potentially worth thousands of dollars for:

- Purchasing new or used electric or hybrid clean vehicles

- Installing residential energy property

- Other environmentally friendly initiatives

There are some restrictions. You’ll want to consult with your tax advisor to determine which credits apply to you.

Work with a financial advisor or use tools

You should consider working with a financial advisor who is well-versed in tax matters. A financial advisor can help guide you on your taxable income. They can also advise you on taxes that might impact your investments.

You can also use any number of tax calculators or tools to speed up the process.

Understanding the nuances of tax laws is essential when it comes to tax planning. This includes personal exemptions. However, you don’t need to stress about understanding these tax laws. No matter what moves you made last year, TurboTax will make them count on your taxes. Whether you want to do your taxes yourself or have a TurboTax expert file for you, we’ll make sure you get every dollar you deserve and your biggest possible refund – guaranteed.

32 responses to “What Is a Personal Exemption & Should You Use It?”